Multi-Asset Perspective – November 2021

29-11-2021

Moderating growth and inflation continue to be key concerns in markets.

Investors have become defensive and high quality securities have become in favor amid the current volatile environment.

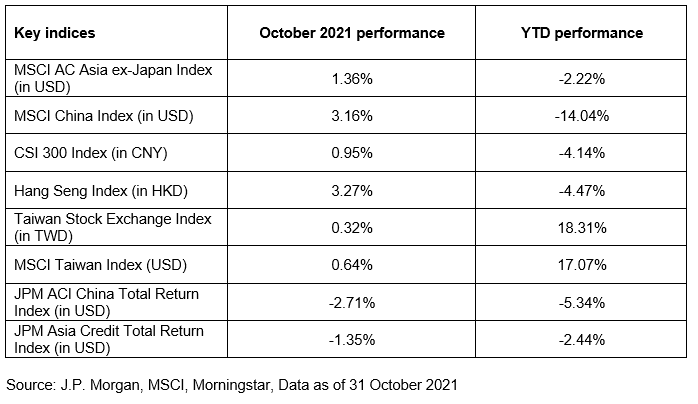

China / Hong Kong equities

- With the market remaining weak, large-cap high-quality companies have become in favor. Concerns over the continued moderating growth in China further dented sentiment, especially in old economy sectors.

- The selloff in the offshore Chinese property bond market continued as several developers missed payment, fueling additional pressure to sentiment.

- On the other hand, Hong Kong’s economy has bottomed with gradual reopening in sight. Hong Kong stocks also acted as a safe haven given the slowdown in China.

China A-Shares

- Analysts continue to downgrade China’s GDP growth forecast for Q4 and next year, while earnings downgrades also continued. Given high raw material prices and the chip supply shortage, companies are facing huge margin pressures.

- However, PPI should have peaked as commodity prices have significantly come down recently. Targeted credit supply has also begun to support selective industries and the credit tightening cycle should have troughed.

Asia ex-Japan equities

- The Fed has started tapering as planned this month, which is expected to last until June next year. The surge in inflation expectations due to rising energy costs, food costs, and wage growth have caused global bond yields to shift upwards, especially at the short end, as global central banks are expected to raise rates earlier. The long ends are fighting between higher inflation but weaker growth.

- Outflows continued from Asia ex-Japan equities as the current macroeconomic backdrop does not bode well for the asset class.

- On the other hand, sentiment in Southeast Asia has improved as markets have started to reopen.

Emerging market ex-Asia equities

- The Fed’s tapering and rising Treasury yields do not bode well for emerging market equities.

- However, as OPEC members remained disciplined on modestly lifting oil supply, oil prices remained elevated, which should support emerging markets, particularly oil-producing countries, in the near term.

Japanese equities

- The lower house election at the end of October was better than expected, with the governing Liberal Democratic Party securing the majority seats. Japan is also making progress with its reopening, and more fiscal stimulus is expected to be out soon.

- Valuations of Japanese equities remain attractive on the back of corporate fundamentals with a good start during the earnings season.

- However, foreign capital is flowing out from the country again and Japan’s GPIF, the world’s largest pension fund, is likely to sell some equities towards the end of the year.

Asia investment grade bonds

- Credit spreads remain tight and may widen as the economy slows down and inflation concerns remain.

- However, as volatility in the high yield space remains high, investors will remain defensive, favoring investment grade bonds.

Asia high yield bonds

- The liquidity concerns on some of China’s property companies have caused a spillover to the whole sector, causing the Chinese property high yield bond space to correct further. With a risk-off sentiment, indicated by investors’ rotation to the defensive areas of the market, Asia ex-Japan high yield credit spreads have widened. We expect that it will take time for sentiment to pick up for spreads to tighten again.

- However, from a valuations perspective, Asian high yield bonds have reached extremely low levels.

Emerging market debt

- Central banks around the world are expected to be more hawkish on the back of rising inflation expectations. With tighter liquidity and weaker EM currencies, investors will remain cautious about emerging market bonds.

- However, as the OPEC remained disciplined on modestly lifting oil supply, oil prices remained elevated, which should give some support in the near term.

Gold

- The strong US dollar and rising Treasury yields do not bode well for Gold.

- That said, over the long term, Gold remains a good hedge against geopolitical uncertainties and would benefit from easing fiscal policies.

Multi-asset

- Multi-asset offers lower volatility compared to traditional single-asset or balanced portfolios. However, the correlation between risk-assets, such as equities, credits, and commodities, has increased dramatically recently. In an uncertain environment with low yields, income becomes an essential source of return for investors.

The author is Kelly Chung, our Senior Fund Manager.

The views expressed are the views of Value Partners Hong Kong Limited only and are subject to change based on market and other conditions. The information provided does not constitute investment advice and it should not be relied on as such. All materials have been obtained from sources believed to be reliable as of the date of presentation, but their accuracy is not guaranteed. This material contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

Investors should note that investment involves risk. The price of units may go down as well as up and past performance is not indicative of future results. Investors should read the explanatory memorandum for details and risk factors in particular those associated with investment in emerging markets. Investors should seek advice from a financial adviser before making any investment. In the event that you choose not to do so, you should consider whether the investment selected is suitable for you.

This commentary has not been reviewed by the Securities and Futures Commission of Hong Kong. Issuer: Value Partners Hong Kong Limited.