2021年︰邁向正常化的一年

04-01-2021

2021年將是經濟重啟之年。疫苗面世,加上市場呈現其他正面消息,全球開始展望疫情陰霾過後的經濟復甦。經濟復甦或會分多個階段進行,而我們認為,圖1概述的明年五大事件及其發展將使投資者的風險胃納延續至2021年。

圖1︰2021年市場更趨穩定的重要事件

資料來源︰惠理基金,2020年12月

疫苗︰經濟復甦的核心

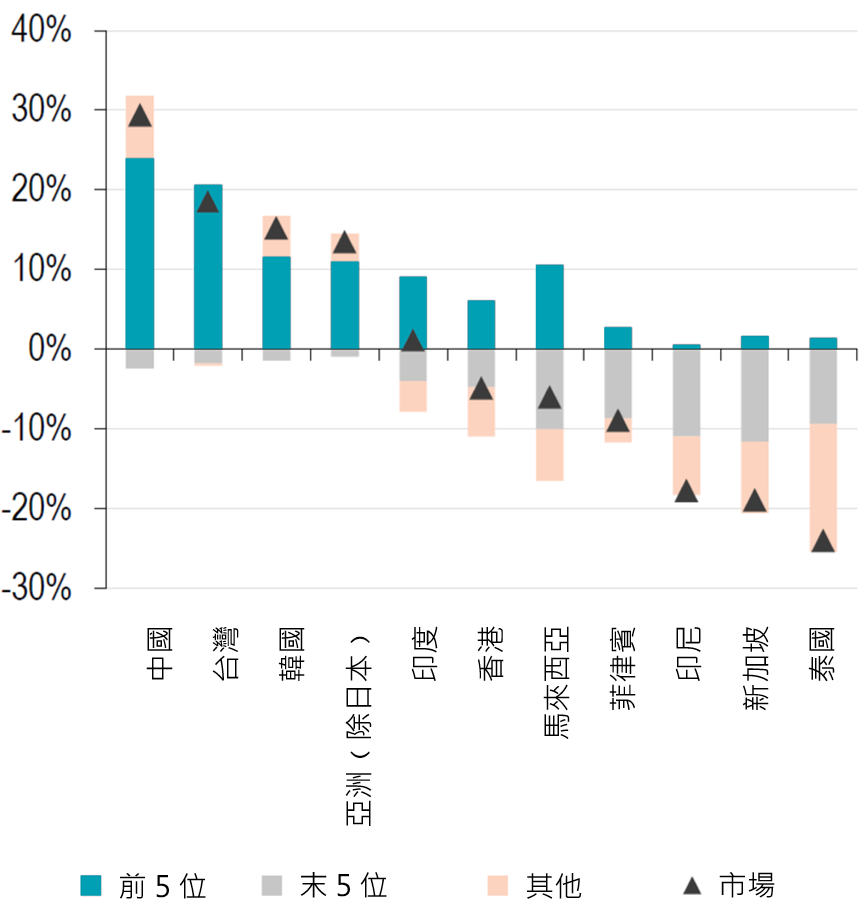

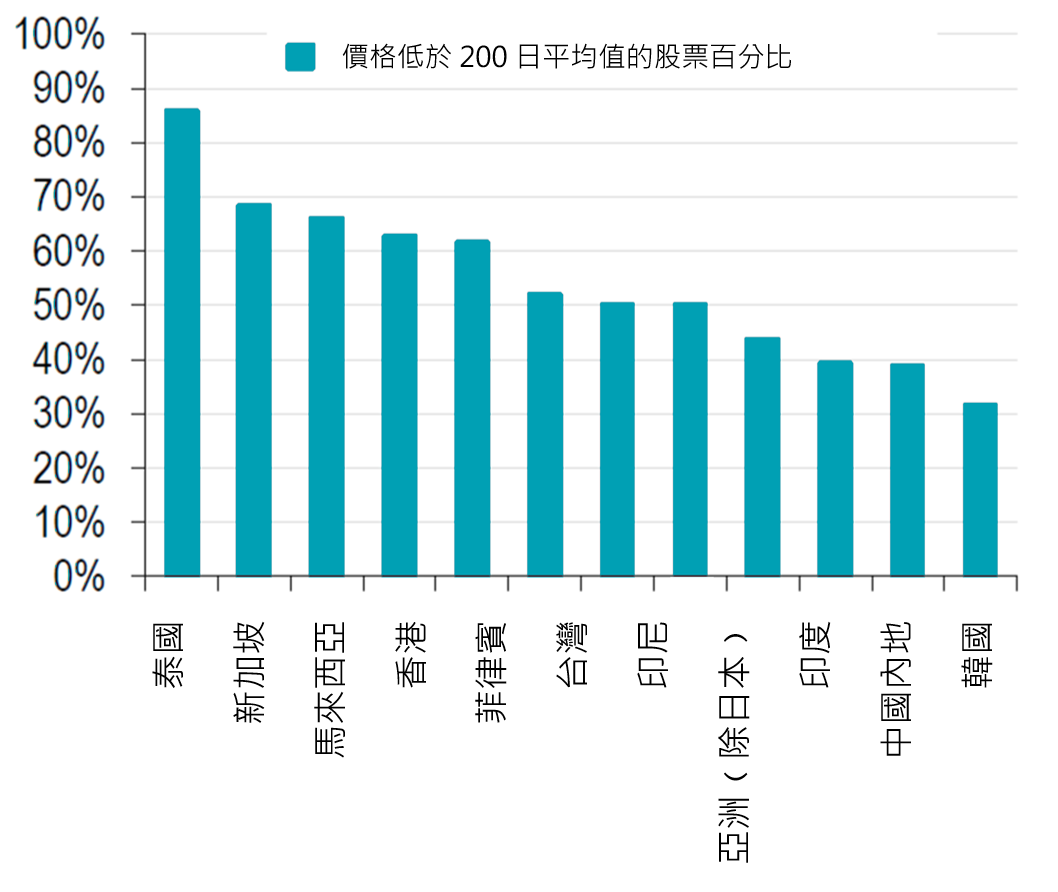

新冠疫情方面,疫苗發展是經濟復甦的關鍵部分,而由於疫苗測試及批准的進度理想,我們認為疫情最壞的情況經已過去。疫苗面世將在2021年大幅推動經濟重啟及復甦。相較2020年,不同板塊的增長匱乏,僅有極少數行業錄得強勁表現﹙圖2a、2b﹚。踏入2021年,金融股及零售股等受疫情重擊的行業將邁進復甦階段,有望帶來更廣泛及平衡的經濟復甦。

圖2a︰2020年亞洲股市表現集中,以位列較前的股份為主

圖2b︰由於不同國家及行業的復甦步伐不一,區內大部分股票表現落後

資料來源︰富時羅素、FactSet、匯豐研究,2020年11月

市場在2020年最後季度對疫苗發展的反應正面,但我們相信僅靠疫苗並不能控制病毒。要徹底杜絕疫情再次擴散,各國必需採取預防措施和有效的邊境控制,並主動為民眾進行測試。此外,接種疫苗的意願、疫苗庫存及成效均會影響疫苗作為經濟復甦的關鍵所帶來的效果。

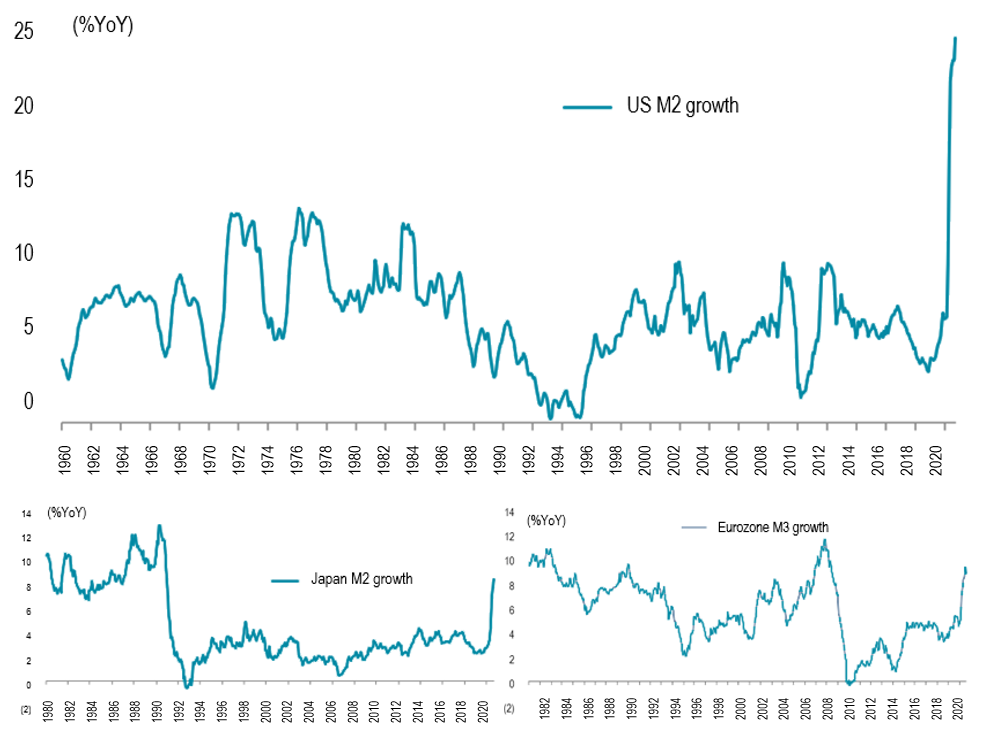

流動性奠定復甦方向

積極寬鬆的貨幣及財政政策是2020年全球股市的主要利好因素,我們預期2021年的投資環境將繼續由流動性帶動。首先,美國聯儲局已表明有意維持較低的借貸成本,情況或持續至2023年。聯儲局前主席耶倫﹙Janet Yellen﹚獲提名擔任財政部長一職,市場認為這表示鴿派取態將會維持,財政支出亦有望增加。

此外,日本及歐洲等已發展經濟體或跟隨美國,甚至以其他方式增加刺激經濟措施,防止其已經脆弱的經濟陷入進一步衰退。全球利率低企,加上流動性充裕,投資者的風險胃納在2021年會維持高漲,我們對股票及高收益債券的偏高持倉正正反映這觀點。

根據歷史,現水平的流動性將使美元走弱,利好新興市場股票。在目前全球均採取寬鬆政策的環境下,中國及個別亞洲市場的經濟復甦領先其他地區,預期將持續吸引資金流入。

圖3︰流動性依然充裕

資料來源︰聯邦儲備局、歐洲中央銀行;彭博、日本銀行;英國財政部、英倫銀行,富瑞

政治衝突得以暫停?

拜登﹙Joe Biden﹚當選總統,局部消除美國大選的相關風險。市場轉而關注拜登政府的內閣班子及新國會下的政策。目前,拜登政府下的中美關係未見明朗,但市場普遍預期,相對過去四年特朗普就任期間,兩國或建立更開放的討論平台。

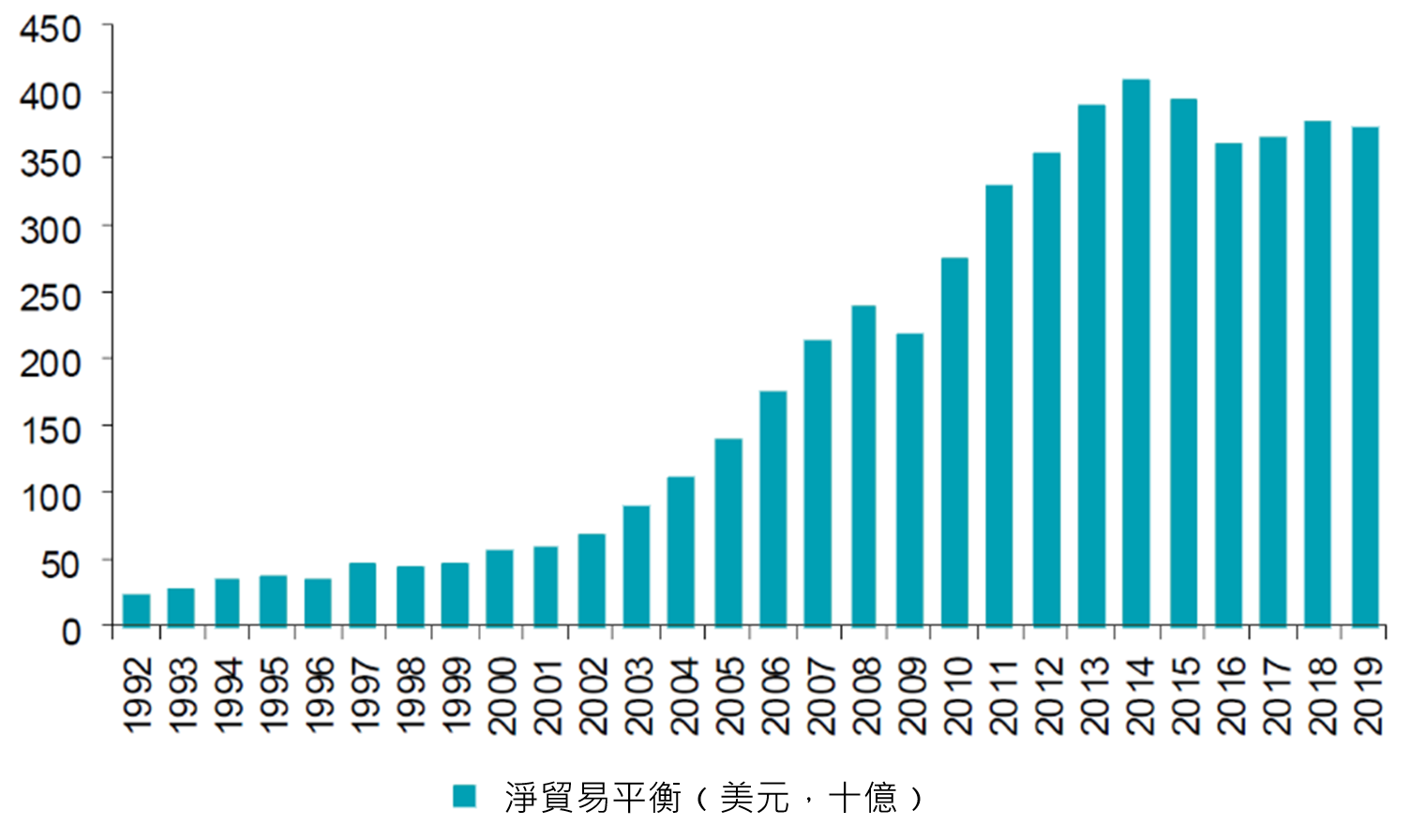

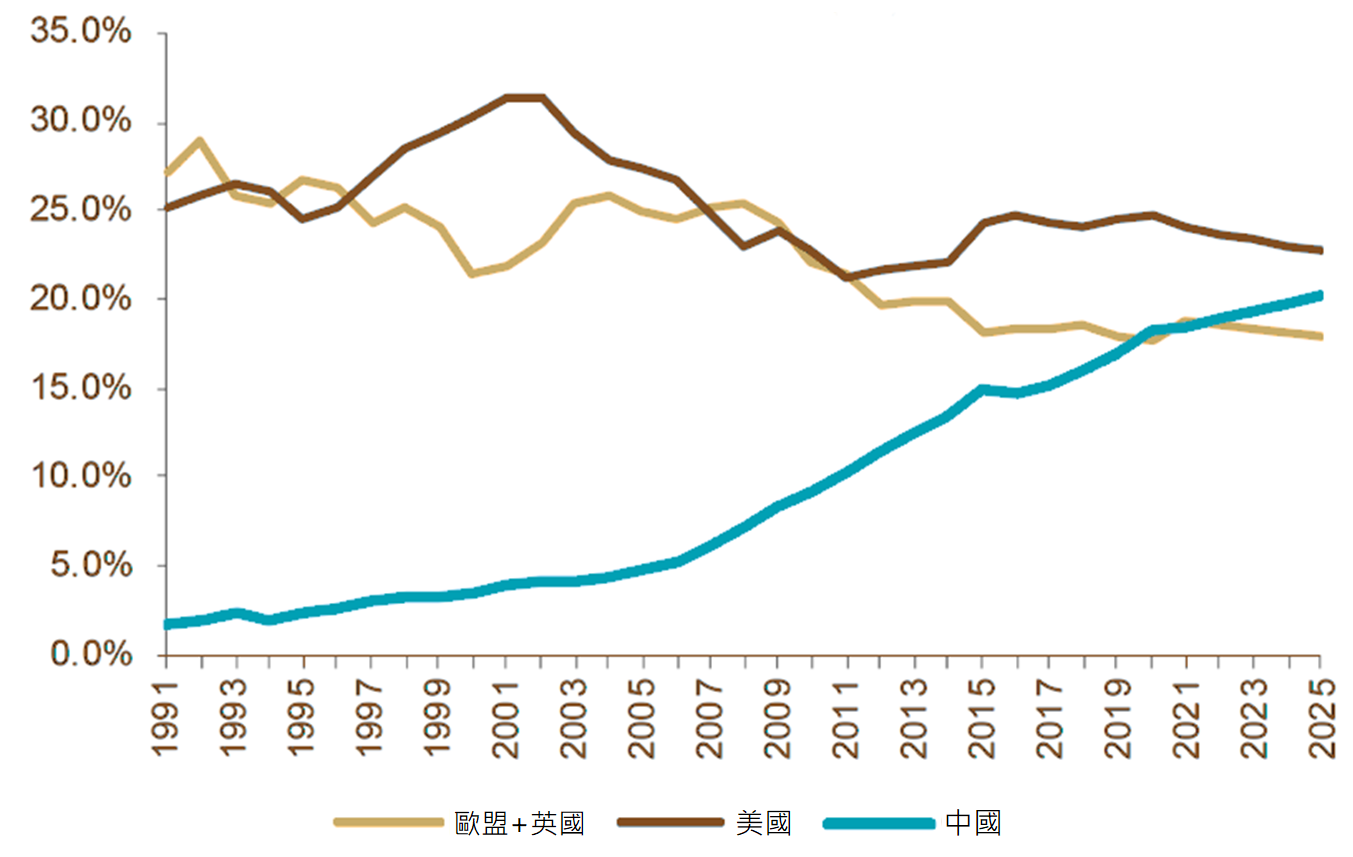

兩國的緊張局面將不會完全消失,我們預計新政府不會完全推翻特朗普政府所實施的政策。過去數十年,中國曾經是世界工廠,以低成本提供勞動力。隨著中國崛起,對全球政治及經濟發揮更大影響力﹙圖4a及4b﹚,同時其在科技等先進的價值鏈領域迅速發展,美國及其西方盟友已重新調整對中國的策略。美國公佈的多個報告表示中國為其策略性競爭對手。因此,制裁及限制措施或會持續,特別是若當局繼續視保護主義為首要的政策方針。

圖4a︰按國內生產總值佔全球份額計算,中國經濟實力超越歐盟及英國總和,即將與全球最大經濟體美國看齊

圖4b︰中國持續錄得淨貿易順差﹙十億美元﹚

資料來源︰國際貨幣基金組織、Comtrade資訊;麥格理研究,2020年12月

中國的五年計劃是國家經濟發展的藍圖,其中,雙循環策略是計劃的核心,亦是對目前地緣政局變化的正面回應。雙循環中的內循環強調本地需求及工業鏈上移至先進製造業的重要性。由於地緣政治風險或將持續,中國將以本地導向的方針作為主要策略,有助減低外部風險觸發的經濟增長波動。

在下一篇投資展望文章,我們將會分析以上事件在2021年的發展,以及諸等因素在亞洲和大中華股債投資市場的啟示。

>> 按此下載完整報告

惠理焦點基金:

免責聲明:

本文提供之觀點純屬惠理基金管理香港有限公司(「惠理」)觀點,會因市場及其他情況而改變。以上資料並不構成任何投資建議,亦不可視作倚賴之依據。所有數據是於呈示之日搜集自被認為是可靠的數據源,但惠理不保證數據的準確性。本文包含之部分陳述可能被視為前瞻性陳述,此前瞻性陳述不保證任何將來表現,實際情況或發展可能與該等前瞻性陳述有重大落差。

本文件並未經香港證券及期貨事務監察委員會審閱。刊發人:惠理基金管理香港有限公司。

致新加坡投資者:本宣傳檔並未經新加坡金融管理局審閱。Value Partners Asset Management Singapore Pte Ltd公司註冊編號為200808225G。